| The HSBC China Services Business Activity Index recording 51.1 in April, down from 54.3 in March, the services survey headline index signaled the weakest expansion of service sector activity since August 2011. Commenting on the China Services and Composite PM data, Hongbin Qu, Chief Economist, China & Co-Head of Asian Economic Research at HSBC said: “The cooling of service sector activity in April likely reflected the knock-on effect of slower manufacturing growth, the impact of property tightening measures and the spreading bird flu. Again, this started to bite employment growth. All these are likely to add some risk to China's growth in 2Q, as there's still a bumpy road towards sustaining growth recovery.” Source by Commodity Insights |

Sunday, 5 May 2013

Economic Buzz: HSBC China Services Index Dips In April

Economic Buzz: Australian Retail Sales Fall In Marc

| The Australian Bureau of Statistics said that Australian retail sales fell to a seasonally adjusted -0.4% in March, from 1.3% in the preceding month. Analysts had expected Australian retail sales to rise 0.2% last month. Source by Commodity Insights |

Saturday, 4 May 2013

Economic Buzz: U.S ISM Non-Manufacturing PMI Registers Slight Increase In April

Economic activity in the non-manufacturing sector grew in April for the

40th consecutive month, said the nation's purchasing and supply

executives in the latest Non-Manufacturing ISM Report on Business. The

NMI registered 53.1 percent in April, 1.3 percentage points lower than

the 54.4 percent registered in March. This indicates continued growth at

a slightly slower rate in the non-manufacturing sector.

Source by Commodity Insights

Source by Commodity Insights

Friday, 3 May 2013

MCX Weekly Review: COMDEX Slips More Than 2%

| MCX Comdex was down by 2.03% to 3466.27 for the week till Thursday. MCX Metal was down by 2.79% to 4379.78 and MCX Energy was down by 1.12% to 3537.60. Bullion: Gold June 13 contract was down by 0.47% to Rs 26914 per 10 grams, Gold M July 13 contract was down by 0.66% to Rs 27042 per 10 grams, Goldguinea May 13 contract was down by 0.73% to Rs 21533 per 8 grams, gold Petal May 13 contract was down by 0.70% to Rs 2691 per gram and Gold Petal Del May 13 contract was down by 0.44% to Rs 2720 per gram. Silver July 13 contract was down by 2.51% to Rs 44633 per kg, Silver M June 13 contract was down by 2.51% to Rs 44668 per kg, Silver MIC June 13 contract was down by 2.50% to Rs 44675 per kg and silver1000 June 13 contract was down by 1.27% to Rs 44288 per kg. Metals: Steel RPR May 13 contract was up by 0.79% to Rs 27910.00 per MT while Aluminum May 13 contract was down by 7.42% to Rs 97.30 per kg, Alumini May 13 contract was down 7.47% to Rs 97.30 per kg, lead May 13 contract was down by 6.97% to Rs 104.80 per kg, Lead Mini May 13 contract was down by 6.93% to Rs 104.80 per kg, zinc May 13 contract was down by 6.36% to Rs 97.90 per kg, zinc mini May 13 contract was down by 6.36% to Rs 97.90 per kg, nickel July 13 contract was down by 5.97% to Rs 810.80 per kg, Nickel M July 13 contract was down by 5.69% to Rs 810.40 per kg, Copper June 13 contract was down by 5.32% to Rs 372.15 per kg, Copper M June 13 contract was down by 5.33% to Rs 372.10 per kg. Energy: Natural gas July 13 contract was down by 5.61% to Rs 223.80 per MMBTU, Brent crude oil May 13 contract was down by 1.91% to Rs 5490.00 per barrel and Crude oil June 13 contract was down by 0.94% to Rs 5046.00 per barrel. Agri Commodities: Cardamom June 13 contract was up by 1.95% to Rs 792.80 per kg, Cotton July 13 contract was up by 0.88% to Rs 18340.00 per bale while Potato July 13 contract was down by 6.70% to Rs 951.20 per 100 kgs, Menthaoil May 13 contract was down by 3.83% to Rs 919.10 per kg, CPO May 13 contract was down by 1.13% to Rs 454.70 per 10 kgs, Kapaskhali May 13 contract was down by 0.35% to Rs 1419.50 per 100 kgs. Source by Commodity Insights |

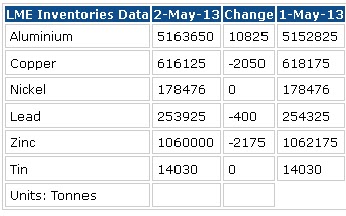

Thursday, 2 May 2013

USDA Estimates Recovery in U.S. Weekly Wheat Exports During April 18-25, 2013

As

per the latest weekly release by the United States Department of

Agriculture ( USDA ) , the weekly U.S. wheat net sales during April

18-25, 2013 were reported at 219,200 MT ( metric tonnes ) for delivery

in the 2012/2013 marketing year were up noticeably from the previous

week, but down 14 percent from the prior 4-week average.

Increases reported for Spain (70,000 MT, including 65,000 MT switched from unknown destinations), Egypt (64,700 MT, including 60,000 MT switched from unknown destinations), Sudan (58,800 MT, including 55,000 MT switched from unknown destinations), Nigeria (46,100 MT, including 14,000 MT switched from unknown destinations), Japan (45,300 MT), and Italy (41,400 MT), were partially offset by decreases for unknown destinations (225,700 MT), Trinidad (13,900 MT), and Honduras (2,000 MT).

Net sales of 497,300 MT for delivery in the 2013/2014 marketing year were primarily for Guatemala (184,000 MT), unknown destinations (100,800 MT), Thailand (55,000 MT), and Mexico (53,000 MT). Exports of 845,200 MT--a marketing-year high--were up 56 percent from the previous and 34 percent from the prior 4-week average.

Source by Commodity Insights

Increases reported for Spain (70,000 MT, including 65,000 MT switched from unknown destinations), Egypt (64,700 MT, including 60,000 MT switched from unknown destinations), Sudan (58,800 MT, including 55,000 MT switched from unknown destinations), Nigeria (46,100 MT, including 14,000 MT switched from unknown destinations), Japan (45,300 MT), and Italy (41,400 MT), were partially offset by decreases for unknown destinations (225,700 MT), Trinidad (13,900 MT), and Honduras (2,000 MT).

Net sales of 497,300 MT for delivery in the 2013/2014 marketing year were primarily for Guatemala (184,000 MT), unknown destinations (100,800 MT), Thailand (55,000 MT), and Mexico (53,000 MT). Exports of 845,200 MT--a marketing-year high--were up 56 percent from the previous and 34 percent from the prior 4-week average.

Source by Commodity Insights

Maize To Extend Correction Though Bargain Hunting Could Emerge Soon

NCDEX

Maize futures could ease further today though some bargain hunting can

emerge in the counter given the recent correction. Maize futures

witnessed some selling in last session. The commodity has mostly been

pressed lower on good supplies in the current week. Market has been

stressed on worries about bird flu in China and higher US stockpiles.

The local arrivals are improving but the production is lower in India

this time around. This could support prices once the peak procurement

period starts in late May-June. NCDEX June futures closed at Rs 1169 per

quintal today, down Rs 7 per quintal or 0.60 % with a 2.30% increase

open interest.

Rabi Maize output is likely to be 15.59 Million Tonnes, down 5.50% over the year. Total Maize output is likely to be 21.06 Million Tonnes, down 3.22%, indicating a shortfall for the commodity on the whole. However, Maize supplies are rising and would keep a tab on prices in near term. The spot prices of the commodity slipped last week towards Rs 1400 per quintal during last week in Delhi.

The spot prices of industrial grade Maize in Delhi have been pushed lower on continued increase in the fresh arrivals of the commodity from Bihar. The increase in arrivals of other grains like Wheat and Barley could also underpin bearish mood in market. Prices are currently at their lowest level in two and a half months.

Source by Commodity Insights

Rabi Maize output is likely to be 15.59 Million Tonnes, down 5.50% over the year. Total Maize output is likely to be 21.06 Million Tonnes, down 3.22%, indicating a shortfall for the commodity on the whole. However, Maize supplies are rising and would keep a tab on prices in near term. The spot prices of the commodity slipped last week towards Rs 1400 per quintal during last week in Delhi.

The spot prices of industrial grade Maize in Delhi have been pushed lower on continued increase in the fresh arrivals of the commodity from Bihar. The increase in arrivals of other grains like Wheat and Barley could also underpin bearish mood in market. Prices are currently at their lowest level in two and a half months.

Source by Commodity Insights

Expecting ECB Rate Cuts Metals Jump To Profits

Copper........

Expecting a slash of interest rates by European Central Bank (ECB) metals are recovering some lost ground. The prices were at multi month lows until yesterday but expected cut of 25 basis points in interest rates by ECB is bringing some hope. Copper tested a 18 month lows on Wednesday and was last seen trading at $ 6911 per tonne, recovering from lows of $ 6897 per tonne.

Yesterday, International Copper Study Group

(ICSG) has reported that the world copper markets were in surplus of

70000 tonnes in January 2013. World mine production of copper in January

was 1467000 tonnes, up almost 14 percent compared to 1290000 tonnes in

January 2012. Mine capacity utilization rates were 82.3 percent in the

month of January compared to 75.4 percent in the previous year.

Yesterday, International Copper Study Group

(ICSG) has reported that the world copper markets were in surplus of

70000 tonnes in January 2013. World mine production of copper in January

was 1467000 tonnes, up almost 14 percent compared to 1290000 tonnes in

January 2012. Mine capacity utilization rates were 82.3 percent in the

month of January compared to 75.4 percent in the previous year.

World refined copper production increased by 1.6 percent to 1708000 tonnes compared to 1681000 tonnes in January 2012. Meanwhile, refined copper usage in World markets declined by 6 percent to 1641000 tonnes in January 2013. The major decline in copper usage was noted in China where consumption fell by 6.8 percent. Chinese apparent net imports were down by 35 percent.

In other metals, Aluminium was trading at $ 1835.5 per tonne, up from $ 1828 per tonne. MCX Aluminium futures for May expiry were trading at Rs 97.9 per kg, up 0.72 percent. The prices tested a high of Rs 98.5 and a low of Rs 97.8 per kg so far in the day. Aluminium is at 31 month low on MCX.

Alcoa announced that it will review 460000 metric tons of smelting capacity over the next 15 months for possible curtailment to maintain the Company's competitiveness, as aluminum prices have fallen more than 33 percent since their peak in 2011. Currently, the company has 13 percent, or 568,000 metric tons of smelting capacity idle.

Nickel prices dipped to a 35 month lows on Thursday and tested a low of Rs 789.8 per kg on MCX platform. The worrying factor is that even after such carnage in Nickel the prices are not in a oversold position. On intraday charts, the sell off can move the metal towards Rs 736 per kg.

Source by Commodity Insights

Expecting a slash of interest rates by European Central Bank (ECB) metals are recovering some lost ground. The prices were at multi month lows until yesterday but expected cut of 25 basis points in interest rates by ECB is bringing some hope. Copper tested a 18 month lows on Wednesday and was last seen trading at $ 6911 per tonne, recovering from lows of $ 6897 per tonne.

World refined copper production increased by 1.6 percent to 1708000 tonnes compared to 1681000 tonnes in January 2012. Meanwhile, refined copper usage in World markets declined by 6 percent to 1641000 tonnes in January 2013. The major decline in copper usage was noted in China where consumption fell by 6.8 percent. Chinese apparent net imports were down by 35 percent.

In other metals, Aluminium was trading at $ 1835.5 per tonne, up from $ 1828 per tonne. MCX Aluminium futures for May expiry were trading at Rs 97.9 per kg, up 0.72 percent. The prices tested a high of Rs 98.5 and a low of Rs 97.8 per kg so far in the day. Aluminium is at 31 month low on MCX.

Alcoa announced that it will review 460000 metric tons of smelting capacity over the next 15 months for possible curtailment to maintain the Company's competitiveness, as aluminum prices have fallen more than 33 percent since their peak in 2011. Currently, the company has 13 percent, or 568,000 metric tons of smelting capacity idle.

Nickel prices dipped to a 35 month lows on Thursday and tested a low of Rs 789.8 per kg on MCX platform. The worrying factor is that even after such carnage in Nickel the prices are not in a oversold position. On intraday charts, the sell off can move the metal towards Rs 736 per kg.

Source by Commodity Insights

Commodities Buzz: ALCOA To Review Smelting Capacity Over Next 15 Months

Alcoa

announced that it will review 460000 metric tons of smelting capacity

over the next 15 months for possible curtailment to maintain the

Company's competitiveness, as aluminum prices have fallen more than 33

percent since their peak in 2011.

The review will include facilities across the Alcoa system and will focus on higher-cost plants and plants that have long-term risk due to factors such as energy costs or regulatory uncertainty. The possible curtailments could affect 11 percent of Alcoa's global smelting capacity. Currently, the Company has 13 percent, or 568,000 metric tons of smelting capacity idle.

“Because of persistent weakness in global aluminum prices, we need to review every option to maintain Alcoa's competitiveness,” said Chris Ayers, President of Alcoa's Global Primary Products. “Any action taken will only be done after a thorough strategic review and consultations with stakeholders.”

When reviewing smelting capacity for possible curtailment, Alcoa will consider a wide variety of alternative actions, ranging from discontinuing pot relining to full plant curtailments and/or permanent shutdowns. Alcoa's alumina refining system will also be reviewed to reflect any curtailments in smelting as well as prevailing market conditions.

Alcoa's review of its primary metals operations is consistent with the Company's 2015 goal of lowering its position on the world aluminum production cost curve by 10 percentage points and the alumina cost curve by 7 percentage points. Decisions on curtailments and/or closures will be announced as reviews are completed.

Source by Commodity Insights

The review will include facilities across the Alcoa system and will focus on higher-cost plants and plants that have long-term risk due to factors such as energy costs or regulatory uncertainty. The possible curtailments could affect 11 percent of Alcoa's global smelting capacity. Currently, the Company has 13 percent, or 568,000 metric tons of smelting capacity idle.

“Because of persistent weakness in global aluminum prices, we need to review every option to maintain Alcoa's competitiveness,” said Chris Ayers, President of Alcoa's Global Primary Products. “Any action taken will only be done after a thorough strategic review and consultations with stakeholders.”

When reviewing smelting capacity for possible curtailment, Alcoa will consider a wide variety of alternative actions, ranging from discontinuing pot relining to full plant curtailments and/or permanent shutdowns. Alcoa's alumina refining system will also be reviewed to reflect any curtailments in smelting as well as prevailing market conditions.

Alcoa's review of its primary metals operations is consistent with the Company's 2015 goal of lowering its position on the world aluminum production cost curve by 10 percentage points and the alumina cost curve by 7 percentage points. Decisions on curtailments and/or closures will be announced as reviews are completed.

Source by Commodity Insights

Commodities Buzz: World Copper Surplus At 70000 Tonnes In January 2013- ICSG

Copper......

International

Copper Study Group (ICSG) has reported that the world copper markets

were in surplus of 70000 tonnes in January 2013. After making seasonal

adjustments the Copper markets was in production surplus of 25000

tonnes. Copper was in deficit of 60000 tonnes in the corresponding

period previous year. The agency has cited that the increase in surplus

has been due to reduction of apparent copper consumption in major

regions.

International

Copper Study Group (ICSG) has reported that the world copper markets

were in surplus of 70000 tonnes in January 2013. After making seasonal

adjustments the Copper markets was in production surplus of 25000

tonnes. Copper was in deficit of 60000 tonnes in the corresponding

period previous year. The agency has cited that the increase in surplus

has been due to reduction of apparent copper consumption in major

regions.

World mine production of copper in January was 1467000 tonnes, up almost 14 percent compared to 1290000 tonnes in January 2012. Mine capacity utilization rates were 82.3 percent in the month of January compared to 75.4 percent in the previous year. Major mine production increases were noted in Chile by 10 percent and in US by 17 percent. Peru which is another major mine producer saw a decline of 4 percent in the mine production.

World refined copper production increased by 1.6 percent to 1708000 tonnes compared to 1681000 tonnes in January 2012. Primary copper production was up by 1.3 percent to 1420000 tonnes in January 2013 compared to 1402000 tonnes last year. Chile which is the second largest producer of refined copper was down by 17.5 percent. China copper production increased by 7 percent in January while a rise of 8.5 percent and 22 percent was noted in Japan and Africa respectively.

Meanwhile, refined copper usage in World markets declined by 6 percent to 1641000 tonnes in January 2013. The major decline in copper usage was noted in China where consumption fell by 6.8 percent. Chinese apparent net imports were down by 35 percent. Excluding China world apparent usage of copper declined by 5 percent. On a regional basis, usage is estimated to have declined by 10% in Africa, by 3% in the Americas, by 6.5% in Asia and by 6% in Europe, while apparent usage is estimated to have increased in Oceania by 20%.

Source by Commodity Insights

International

Copper Study Group (ICSG) has reported that the world copper markets

were in surplus of 70000 tonnes in January 2013. After making seasonal

adjustments the Copper markets was in production surplus of 25000

tonnes. Copper was in deficit of 60000 tonnes in the corresponding

period previous year. The agency has cited that the increase in surplus

has been due to reduction of apparent copper consumption in major

regions. World mine production of copper in January was 1467000 tonnes, up almost 14 percent compared to 1290000 tonnes in January 2012. Mine capacity utilization rates were 82.3 percent in the month of January compared to 75.4 percent in the previous year. Major mine production increases were noted in Chile by 10 percent and in US by 17 percent. Peru which is another major mine producer saw a decline of 4 percent in the mine production.

World refined copper production increased by 1.6 percent to 1708000 tonnes compared to 1681000 tonnes in January 2012. Primary copper production was up by 1.3 percent to 1420000 tonnes in January 2013 compared to 1402000 tonnes last year. Chile which is the second largest producer of refined copper was down by 17.5 percent. China copper production increased by 7 percent in January while a rise of 8.5 percent and 22 percent was noted in Japan and Africa respectively.

Meanwhile, refined copper usage in World markets declined by 6 percent to 1641000 tonnes in January 2013. The major decline in copper usage was noted in China where consumption fell by 6.8 percent. Chinese apparent net imports were down by 35 percent. Excluding China world apparent usage of copper declined by 5 percent. On a regional basis, usage is estimated to have declined by 10% in Africa, by 3% in the Americas, by 6.5% in Asia and by 6% in Europe, while apparent usage is estimated to have increased in Oceania by 20%.

Source by Commodity Insights

Subscribe to:

Posts (Atom)